Hello, hope you’ve had a great week.

| |

|

|

|

|

|

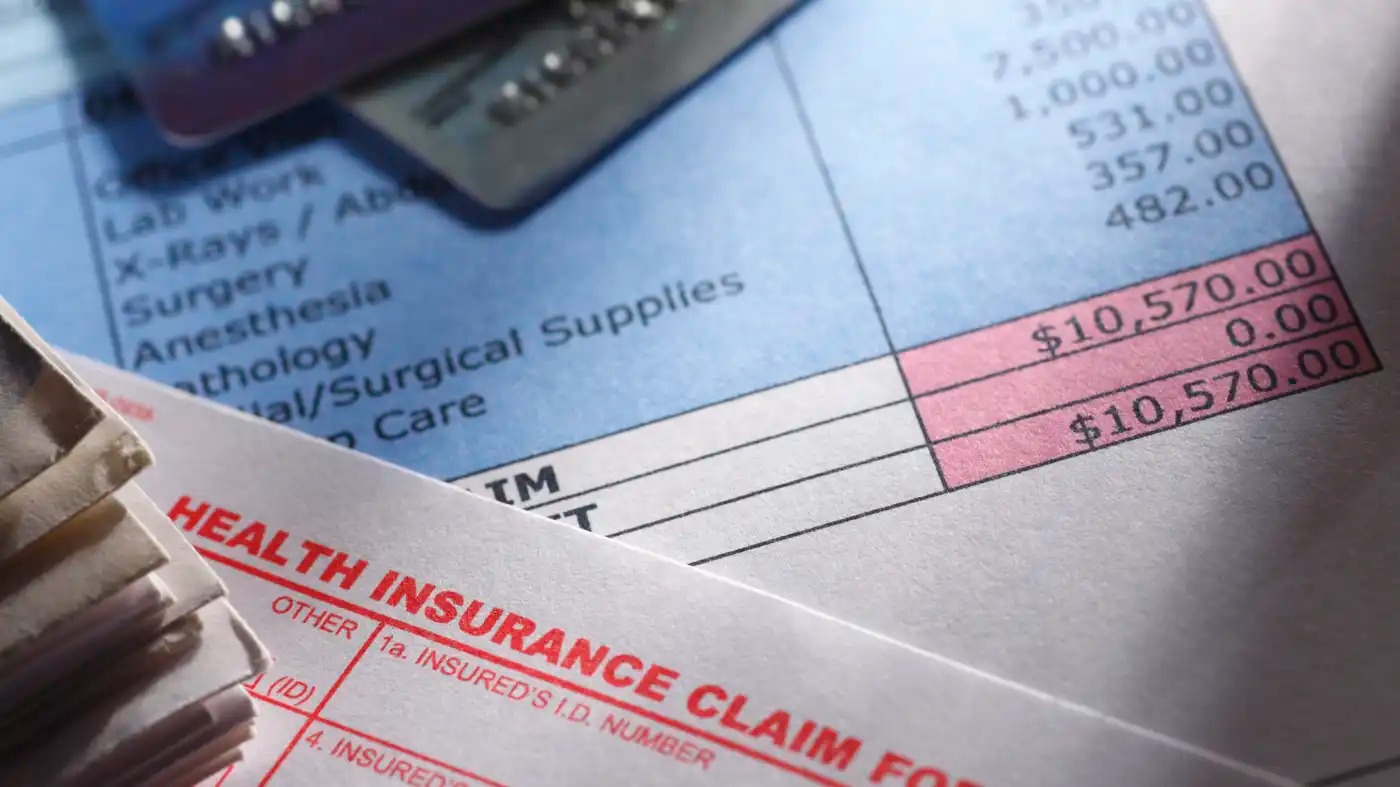

Getty Images | Catching errors by insurers is a growing industry |

Employers are turning to independent companies to catch medical billing mistakes and recover their money. Alexandra Olgin reports |

Most employers, two-thirds, pay their own healthcare bills. They just hire insurers to do the logistics. They expect insurers to check claims to find mistakes and overpayments. But it’s not their money, and there’s no incentive to closely monitor the dollars.

That’s where so-called payment integrity companies come in. The mistakes they find are saving employers anywhere from 5% to 15% of their annual healthcare spend.

It’s a well-accepted fact that many medical bills have errors, and employers expect that the insurers they pay to run their health plan would catch them. Turns out that’s a bad assumption, said Joanne Hinton. She ran health benefits for the 12,000 Fort Worth employees, family members and retirees in Texas until April.

“I think we were ignorant,” Hinton said, “It's kind of the: what you don't know, that you don’t know.”

In 2017, Hinton found that Aetna, the city’s insurer, double-paid a $450,000 medical claim. “We were fighting them, because why did you pay this twice?” Hinton said, “That's our money. Get it back.”

She wondered how many other mistakes Aetna was making and how much it was costing Fort Worth.

“Any dollar that we spend on healthcare is a dollar we are not spending on roads, traffic lights, firefighters, parks,” Hinton said. “It's really important for us as a governmental entity to make sure that we are spending the money correctly.” | |

|

|

|

|

| Take the Marketplace news quiz! | | Listen to “Marketplace,” test your knowledge, brag to your friends. | |

|

|

|

|

Kristin Schwab/Marketplace |

Adults are spending big on toys |

Marketplace’s Kristin Schwab reports "kidulting" is fueling growth in the toy market. |

|

To the uninitiated, a Labubu is kind of a hard thing to explain. The figurine — a creature with pointy ears and mischievous grin — is part bag charm, part collectible, part fashion trend.

“I saw it online and I was like, ‘Oh my god. What is this?’ Almost was, like, is this supposed to be something cute?” said 27-year-old collector Douglas Estelle. “You know what I mean. I was like, ‘Oh my god it’s, like, adorable.’”

“I have all the pendants, all the plushes. I love the plushes, they’re like my everything,” said Estelle, who’s spent more than $2,000 collecting a few hundred Labubu dolls, including oversized versions, which can stand as tall as five feet. “Labubu is always there for me. I love her so much.”

Despite worries about the rising cost of living, people are pouring money into discretionary spending like toys. Consumers 18 and older accounted for 35% of the toy industry’s growth

in the first four months of this year, according to a recent report by market research firm Circana. Toys have become so popular for adults that the industry has come up with a new term for it: kidulting.

“I did not coin this phrase, by the way,” said Brian Spaid, a marketing professor at Marquette University who researches collecting. “This is really about people giving themselves permission to kinda get in touch with their inner child, go back to their childhood, enjoy the things that they enjoyed as kids.” | |

|

|

|

|

| Here are the stories readers clicked on the most in our Daily Wrap newsletter this week. Sign up to get the latest news and numbers in your inbox every weekday evening.

| |

|

|

|

|

|

Delaware State University via Getty Images | Why did so many legacy companies use the word "general"? |

A listener wanted to know why General Motors, General Electric and General Mills are called that. Marketplace’s Janet Nguyen asked around. |

|

The modern business landscape often prizes wacky, unusual names and will accept — even embrace — misspellings. Think Google, Crumbl Cookies and Poppi. But in the late 19th century and early 20th centuries, it was actually a virtue to be as plain as possible.

Marketplace spoke to U.S. business historians and economists who, overall, say they're not aware of why exactly companies like General Mills and General Electric chose the word "general."

But they offered several theories for why they may have chosen the term. The naming convention simply could've become the norm for major corporations who wanted to shake off their regional identities after a merger. Companies could have also chosen general terms because they wanted to distance themselves from their rich owners at a time when there were extreme wealth disparities in America. Or they may have wanted to signal how much potential the company had.

Jennifer Black, a historian, said she thinks the term wasn't a "deliberate branding choice," but a cultural trope that arose out of the merger movement in the 1890s.

"In the 1890s, you really see a consolidation of companies in the United States, with several mergers happening across the board," said Black, who's a professor at Misericordia University and the author of the book "Branding Trust: Advertising and Trademarks in Nineteenth-Century America."

It occurred in a variety of industries, but many of these mergers were happening in "corporate, consumer-oriented industries," Black explained.

Let’s run them down. | |

|

|

|

|

| |

SONG OF THE WEEK |

"No One Lasts Forever Featuring David Cronenberg" by Charli xcx |

|

| |

|

|

|

|

|

The biggest pop stars produce multiple special edition vinyl records with alternate album art, cool colors and bonus material. Fans will often snap up multiple copies,

subsidizing all us casuals. One problem: The albums aren’t always done by the time the records need to be pressed, so the “real” album is only available on streaming services, which can push out releases on short notice.

Olivia Rodrigo and Raye shipped incomplete records to fans earlier this year, the Guardian reports, and Charli xcx’s “Music, Fashion, Film” is the latest album to be reshaped by the shortened streaming timeline. | |

|

|

|

|

|

Thanks for reading! If you enjoyed this newsletter, forward it to a friend. If this newsletter was forwarded to you,

subscribe to Marketplace newsletters here.

Got feedback for us? Just reply to this email. We can't get back to everyone, but we read it all. | | |

| |

|

|

|